When this “everything bubble” bursts the cascading events will no doubt make 1929 look like a Sunday school picnic by comparison. This time around, the underlying fundamentals are exponentially worse.

1929 was a kleptocratic orchestrated pump-and-dump con too, but the amount of underlying debt held in those days by individuals, businesses, commercial banks, central banks, and sovereign treasuries, was utterly minuscule by comparison.

This time around the global debt is somewhere between $350-400 trillion which makes it ~400% of global GDP. This figure alone makes it a mathematical certainty that the global Ponzi scheme will unravel… spectacularly!

Furthermore, the world derivative market is now estimated to be in the vicinity of $2.4 Quadrillion… yes that’s a great big fat Q… each Q = $1000 trillion. This utterly mind-boggling total is around 26 times global GDP. These are all casino bets. Financial derivatives are debt bets.

Some claim that this is no big deal because the $2.4 Quad is a notional total – IOW two sides of the same bet added together. OK, but halving that $1.2 Quad is still a fair stack of coin nevertheless. Derivatives basically just mean that one party bets that an underlying asset will go up in value and the other side bets it will go down… a zero sum game right?… WRONG!

That all works fine until one side of the debt bet loses so badly that they can’t pay the winner, which means both sides are suddenly losers. When this begins to happen and the contagion dominoes through in an illiquid financial environment things get messy real quick. The rot set way back in the 90s (on Slick Willy’s watch) when the Glass Steagall act, which had kept client deposits out of the hands of the big bank speculators, was repealed and everything including depositors’ funds became part of the casino.

But wait, the story gets far worse – after the Cyprus crisis bank run, we were all sold yet another crock. The West all piled into signing up to a new way of handling financial events like this. It was brokered to Mainstreat, dressed up like a pig covered in lipstick – where no longer would banks be bailed out by the Treasury (AKA you and I) but instead would be on their own and could regain liquidity by using bail-ins – IOW using depositors funds to provide much-needed liquidity. within the institution itself.

Of course part of this danger was already there anyway, because depositors are always the lowest-ranking creditors – they are in effect completely unsecured – IOW you rank even below derivatives when it comes to divvying up in a financial meltdown or patching up a liquidity crisis.

The problem this week is that this should be wake-up for depositors the world over. In effect the latest bankrun is now a huge bullhorn echoing globally and waking people up to the fact that, as depositors in banking institutions, they are all unsecured creditors.

In the event of a systemic meltdown, word is getting out now that there is no way that the system can be propped up, because even using bailouts the amount of funds required would overwhelm the treasury.

The truly gobsmacking realisation now needs to dawn too – there are no longer any magic wands and this coming event is far beyond the combined powers of both the Treasury and the Fed to be able to patch up. Take out all of the multitude of bewildering acronyms and financial jargon, and this situation is actually no more complicated than basic high-school maths.

The US Treasury is currently insolvent to the tune of $31 trillion, and the Fed is ~$1 trillion in hock. This is before a cascade of asset bubbles starts popping. This time the mounting subprimes lurk around every corner. Just the occupancy rates on commercial office buildings alone are a disaster waiting to happen. Occupancy rates are estimated to be only 50% in the big centres, and around that figure also on a national basis. What happens when the owners of these run out of liquidity… this will be another giant asset bubble burst.

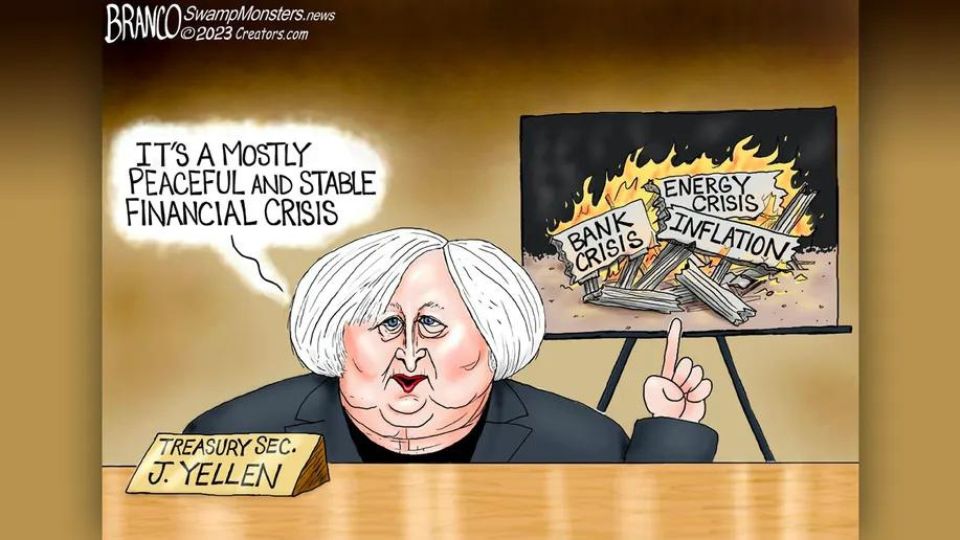

I would hazard a guess that the horrible little hag that “runs” the Treasury and the utterly gormless J Powell, the hopeless talking head of the NY Fed, will be in full-scale panic mode today. Simply put, neither of these utterly incompetent institutions has the power to save the US dollar AND the financial system. They have to choose between one and the other… this is a rock and a hard place moment.

If they try to save the financial system there will be capital flight which means the US$ weakening and rampant inflation. This will be exacerbated even more now because the BRIICS+ are on the cusp of finalising a new hard-backed reserve currency instrument that would offer a haven for capital flight both in terms of safety and stability.

The US in this scenario loses its extraordinary privilege where it can buy stuff and pay for it simply by printing funny money out of thin air. This will result in hyperinflation because the US no longer produces the everyday items they require… this will result in a huge drop in living standards and almost certain social mayhem.

THE CHOICES… a rock or a very hard place indeed

#1 Save the financial system… meaning having to loosen because they have tightened far too hard and fast in a farcically overleveraged financial casino… THESE ARE THE MOST HIGHLY LEVERAGED FINANCIAL MARKETS IN ALL OF HISTORY… WTF did these retards think was going to happen?

#2 Save the dollar… but to do this they have to keep interest rates high and keep tightening = destroying the US economy.

The rot set in majorly with the repeal of Glass Steagall in the 90s but the U$ then proceeded to bet the entire farm on this giant Ponzi scheme, when they undertook (pun intended) the huge bailouts in 2008. FDIC insurance is farcically inadequate now in a systemic failure with runs on banks. In terms of insuring total deposits their funds probably only amount to ~5% of cover.

Balance sheets of banks and central banks are also misleading when they show bonds as assets ‘marked to maturity’ as opposed to ‘marked to market’ This is OK if they have the liquidity to hold them to maturity and can retrieve their value 100 cents in the dollar… but not if they have to cash them in at lower values like 70-80 cents in the dollar. This distortion of balance sheets is manifest worldwide. With bank runs escalating and institutions desperately having to find liquidity, these banks can quickly become insolvent within days.

Also, if they do choose #2 and defend the dollar this will likely bleed into derivatives and a cascade of defaults. Some very reliable commentators think that they will have to choose #1 and let the dollar burn. This comes down to a fundamental maxim in fiat Ponzi schemes… INFLATE OR DIE… period.

Maybe we need a new maxim… DIE OR DIE… those are the only two choices I see – kind of like facing the firing squad at dawn and the head executioner very obligingly enquires as to what calibre of rifle you would like them to use.

Now how does the old adage go that we could use to describe the US financial Ponzi – is it something like this…?

“Well, I’d say it is f$%$ed wouldn’t you”?

My sneaking feeling is that the oligarchs knew that a black swan would appear which would be the precursor to having to make the above ‘choice’. I’m not confident about which way they will go. I would lean towards a feckless panicked blend of components from both #1 and #2.

The other giant elephant in the room is the massive paper manipulation used to control gold and silver prices in order to help protect the fiat currencies. These market manipulators will no longer be able to afford to beat down the physical price with paper shorts.

On Friday last week, there was still supply in most dealers in the U$ but this could change in a flash. Once failure to supply events hit the physical gold markets could go ballistic almost overnight. This would then signal the death knell for all fiat currencies. In a matter of days, these PMs could be impossible to purchase regardless of their token price.

Powell and Yellon have to be in full panic mode now, as the puppet masters above them try to use this combination of events to con Mainstreat into accepting CBDCs by fast-tracking the Citibank, and Wells Fargo hybrid wholesale CBDC trial, into full customer retail accounts at the Fed.

This would mean that the private cartel-owned TBTF banks (which are technically insolvent anyway) would be unceremoniously thrown under a very large Wall Street bus.

Take that Mr Dimon, you crazy diamond. How’s your shine going for you so far this week?

Cheers to all (except banksters)